The Federal Reserve has officially cut interest rates by 0.50%, and while that headline sounds like good news, the real question is this:

What does this rate cut actually mean for your money?

More specifically:

- Should you refinance your mortgage?

- Is now a good time to buy a car?

- Will credit card debt finally get easier to manage?

In this breakdown, we’ll walk through how the Fed’s rate cut impacts housing, auto loans, and consumer debt, and—more importantly—how to make wise financial decisions instead of costly emotional ones.

Understanding the Fed’s Interest Rate Cut

The Federal Reserve does not directly control mortgage rates, car loan rates, or credit card rates. Instead, it sets a benchmark rate that influences how expensive borrowing becomes throughout the economy.

Historically, rates rise fast—but they fall slowly.

To put things into perspective:

- In 2021, 30-year mortgage rates hovered around 3%

- By 2022, they doubled to 6%

- In 2023, rates peaked near 8%

- Today, we’re hovering closer to 6%, with projections near 5.7% by next year

The key takeaway? Waiting for “perfect” rates often costs more than acting wisely at “good enough” rates.

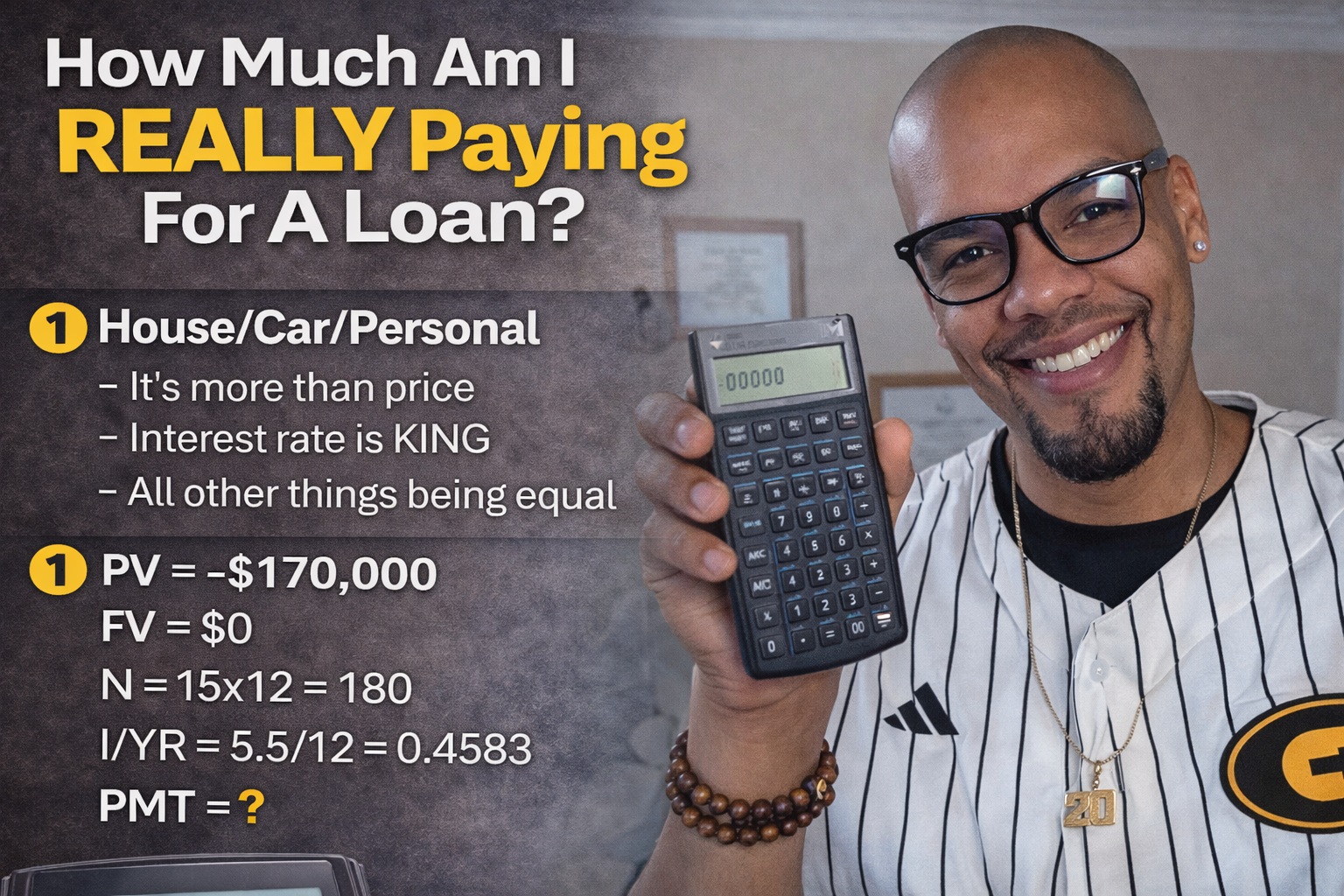

Mortgage Rates: Should You Refinance or Buy Now?

If you already own a home or are considering buying one, this rate cut presents both opportunity and risk.

The Biggest Mortgage Myth: “I Don’t Want to Restart a 30-Year Loan”

One of the most common mistakes homeowners make is assuming that refinancing means starting over with a new 30-year mortgage.

That’s simply not true.

If you’ve already paid:

- 15–20 years into your mortgage

You can refinance into: - A 10-year or 15-year loan

- Potentially lower your interest rate

- Pay less total interest over time

Refinancing is not about extending debt—it’s about optimizing it.

Opportunity Cost Matters More Than Timing the Fed

Many homeowners waited for rates to “go even lower” over the last few years. Instead, rates spiked, inventory tightened, and refinancing opportunities disappeared.

This is called opportunity cost.

If refinancing saves you thousands—even after closing costs—it may be worth acting instead of waiting for a hypothetical future rate cut that may never materialize.

Buying a Home When Inventory Is Low

Housing inventory remains tight, which means competition is still fierce.

If you’re planning to buy:

- Improve your credit score

- Avoid opening new credit lines

- Pay down high-interest debt

- Get all financial documents organized

- Work with an experienced real estate agent

Waiting an extra year for a slightly lower rate may cost you the house you actually want.

Sometimes the best financial decision is buying the right asset at the right time—not chasing the lowest possible rate.

Car Loans: How to Avoid Overpaying on the Back End

Car prices are falling, incentives are returning, and inventory is improving—but loan rates remain elevated.

Current averages:

- New car loans: ~7%

- Used car loans: ~11%

Here’s the most important rule when buying a car:

Always Get Pre-Approved Before Going to the Dealership

Dealerships often mark up interest rates and earn money on the back end of the loan.

How to protect yourself:

- Go to your bank or credit union first

- Get a pre-approved rate

- Do not disclose that rate upfront at the dealership

- Negotiate the vehicle price first

- Only reveal your rate at the end

This single step can save you thousands of dollars over the life of the loan.

Credit Card Debt: The Most Dangerous Impact of High Rates

Credit card interest rates are at historic highs:

- 23% for new cards

- 21% for existing balances

That means a $100 purchase can quickly become $123—or more.

Smart Strategies to Pay Down Credit Card Debt

If you’re carrying high-interest debt:

- Pay off the highest-interest cards first

- Consider a 0% balance transfer (if your credit qualifies)

- Explore a personal loan with a lower fixed rate

But here’s the warning most people miss:

If your credit score is already damaged or your cards are maxed out, many of these options won’t be available to you.

Credit matters most before you’re in trouble—not after.

The Hidden Option: Credit Card Hardship Programs

If you’re struggling, many credit card companies offer hardship programs:

- Temporarily freeze your card

- Lower your interest rate

- Allow structured repayment for 3–9 months

These programs are not advertised—but they exist.

Always ask.

The Biblical and Financial Principle at Work

Debt is not just a math problem—it’s a stewardship issue.

Paying back what you owe:

- Protects your credit

- Preserves future opportunities

- Frees you to invest and build wealth

- Aligns with biblical principles of integrity and responsibility

Every dollar not paid in interest is a dollar that can compound for your future instead of enriching lenders.

Final Thoughts: Save More Than You Spend

As we move into the holidays, remember this truth:

Debt-free living is the best gift you can give yourself.

Save more than you spend.

Plan before you borrow.

Negotiate everything.

And don’t let fear or greed dictate your financial decisions.

Need Help Making Sense of It All?

If these strategies feel overwhelming, you’re not alone.

For a simple, faith-based introduction to money management and retirement planning, check out The 4 Pillars to Christian Investing—a beginner-friendly guide covering:

- 401k planning

- Debt management

- Savings strategies

- Investing and wealth transfer principles

Written by A.B. Ridgeway, CPWA®, with over a decade of experience helping families live lives that are rich and righteous.

If you found this helpful, share it, subscribe, and continue learning how to steward your finances wisely.

I’ll see you on the other side of your blessing.

About the Author

A.B. Ridgeway, CPWA® is the founder of A.B. Ridgeway Wealth Management and host of The Ridgeway Report. He specializes in helping retirees and pre-retirees create reliable income, invest with clarity, and make confident financial decisions.

Join our Newsletter and receive our free 19-page e-book “4 Financial Principles Every Christian Should Know”

Click Here To Get Your Free Gift

About The Ridgeway Report:

As Christians, we were taught to be good stewards over our tithing and giving to the less fortunate. But when it came to our personal finances and investing we were left clueless on what the Bible says. What does the Bible say about managing debt, leaving a legacy, investing, and planning for your retirement? Mr. Christian Finance answers these and many other questions because we want to teach you how to become rich and righteous!

Meet A.B. Ridgeway:

A.B. Ridgeway, MBA, CPWA®️ (info@abrwealthmanagement.com) is the owner and Christian Financial Advisor with A.B. Ridgeway Wealth Management. With a decade in the finance industry, his goal is to give believers clarity around the most confusing topic in the Bible, money, and tithing. A.B. Ridgeway helps tithing Christians become cheerful givers but unlocking their money-making potential, so they can prosper and be the great stewards of the wealth God has entrusted them with.

*Disclaimer: This communication is not intended as an offer or solicitation to buy, hold or sell any financial instrument or investment advisory services. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy or the completeness of any description of securities, markets or developments mentioned. This is strictly for information purposes. We recommend you speak with a professional financial advisor.

*Some elements in this blog was created, restructured, edited or summarized by AI and may have altered from the original content. Warning: There may be errors that were creating during this transition that were not in the original content. Please double check all information.