Still Investing Like You’re 40? Why It Can Destroy Your 401k in Retirement

If you are planning to retire soon—or you’ve already retired—this is one of the most important conversations you can have about your money.

A.B. Ridgeway Wealth Management

If you are planning to retire soon—or you’ve already retired—this is one of the most important conversations you can have about your money.

Understand 401k withdrawal rules in retirement, how much you can withdraw, tax implications, and strategies to avoid costly mistakes with your retirement account.

Americans are increasingly cashing out their 401ks, often unaware of the long-term consequences. Rising debt pressures, lack of emergency savings, and confusion during job transitions lead many to raid their retirement funds for urgent expenses. Financial advisors stress the importance of preserving wealth through careful planning and professional guidance.

Thinking about stopping your 401k contributions? Here’s what to know about match rules, fees, and professional guidance before you change anything.

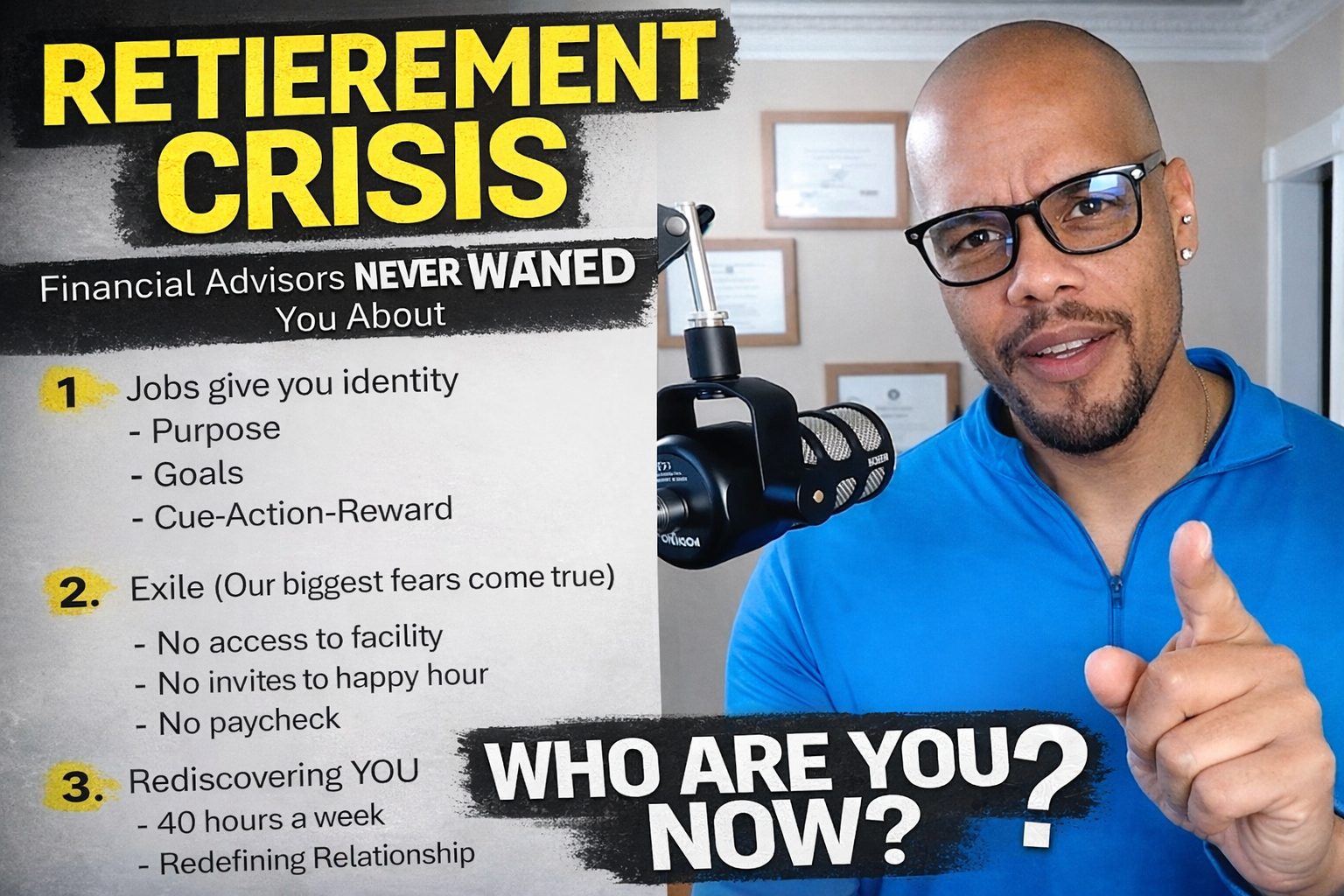

Retirement isn’t just about money. It’s about identity, purpose, and meaning. Learn how to prepare emotionally, spiritually, and financially for life after work.

The article addresses misconceptions about 401k retirement accounts, clarifying that they are not scams but tax-deferred tools for saving. It highlights the importance of understanding tax implications, managing accounts properly, and considering rollovers to optimize retirement outcomes. Working with a financial advisor is essential for informed decision-making and avoiding costly mistakes.

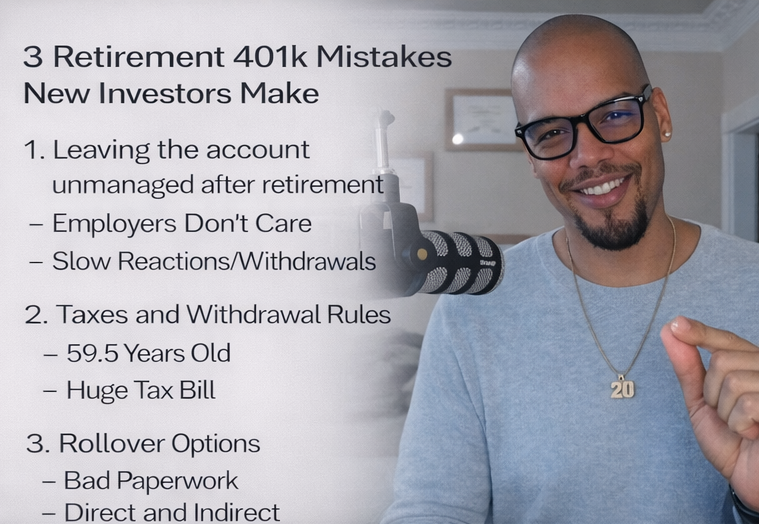

When leaving a job, many Americans forget about their unmanaged 401k, risking financial loss. Common mistakes include not understanding tax implications, withdrawal penalties, and rollover options, which can result in costly penalties and delayed access to funds. Properly managing a 401k is essential for financial security in retirement.

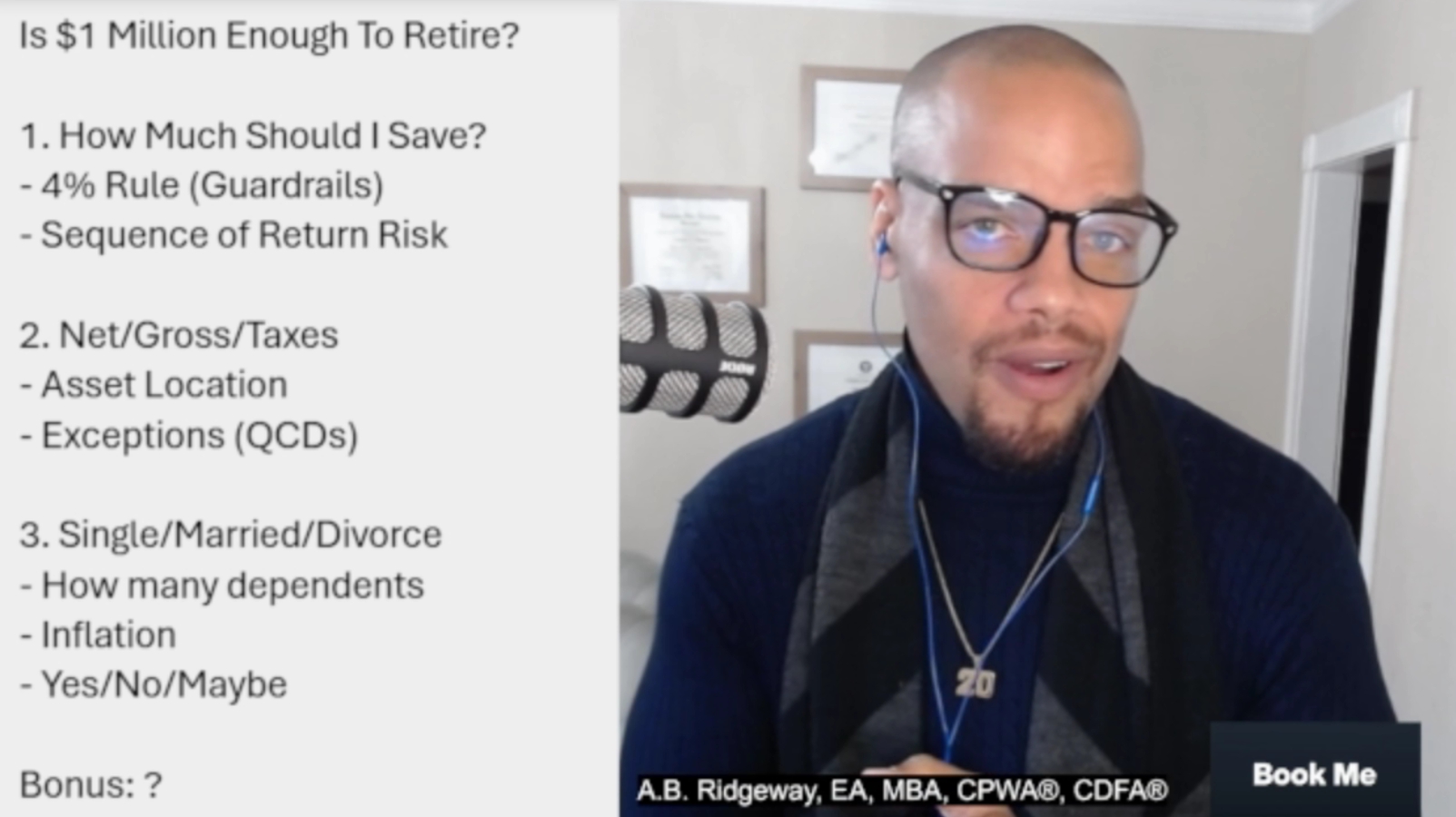

The perception that $1 million ensures a comfortable retirement is outdated due to rising costs and increased longevity. Retirement planning should focus on individual lifestyle needs rather than an arbitrary figure. Factors like the 4% rule, taxes, asset location, and personal circumstances are critical to determining financial readiness for retirement.

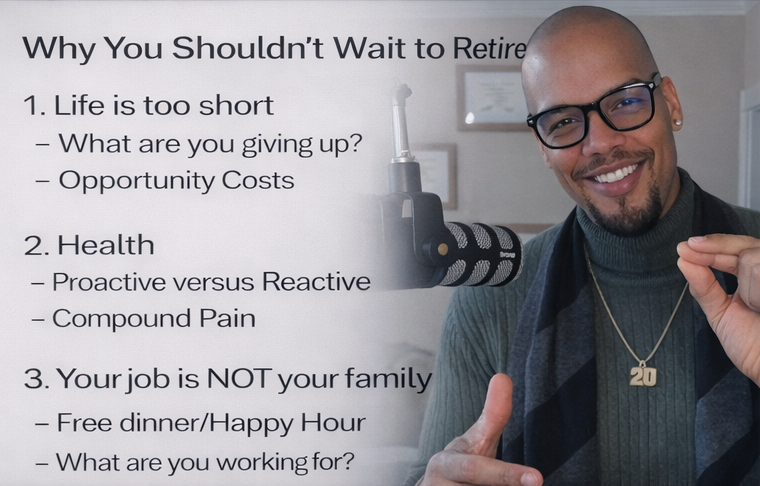

Retirement is a deeply personal choice influenced by factors beyond finances, including time, health, and relationships. Delaying retirement can lead to lost opportunities and diminished health. It’s crucial to assess what “enough” means for your lifestyle, making retirement a deliberate decision rather than a default. Planning can ease stress and clarify options.

A.B. Ridgeway discusses the importance of calculating retirement income paycheck accurately to ensure financial stability. Using assumptions like inflation and rate of return, he demonstrates that one would need approximately $316,696.71 to withdraw $45,000 annually for eight years. Seeking expert financial advice is essential for effective retirement planning.